Up, Up and Away

Singapore's Miraculous (and Dangerous?) Property Market

In the past decade it has been common place to observe that China’s had a property bubble and that in 2022 or so it rapidly deflated through a combination of factors including leverage mountains, Zero Covid effects on the economy and buyer psychology and policy action.

This was and is concerning because the property market represented an unhealthy 24 to 30 percent of annual GDP, which was toxic levels when the supporting debt load as well as the economic unproductivity are considered.

In the case of Singapore the real estate sector represents some 10 percent (although official figures are vague) of annual GDP. Sounds reasonable? Not when this is considered as a share of just domestic GDP - which is 25 percent of total GDP.

In which case, the magnitude is multiplied by 400 percent. In other words, the real estate sector is plausibly 40 percent of domestic GDP. This is without factoring the governments substantial capex spend.

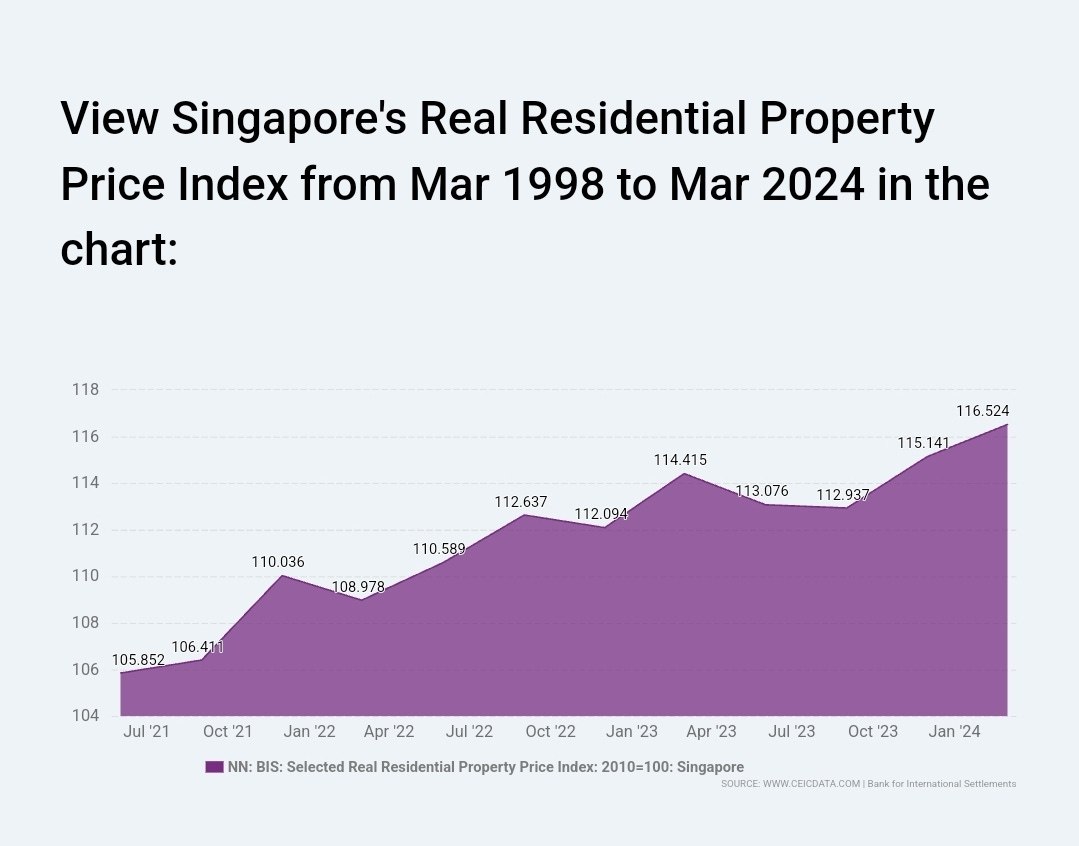

The ever rising prices, despite 8 rounds of cooling measures, Covid 19 and geopolitical and macroeconomic shocks is remarkable and should warrant greater policy scrutinity.

With real estate representing the largest asset on household balance sheets and debt loads rising in relation to movements in market prices.

Now consider that construction - particularly in real estate - has always been notoriously unproductive - while consuming vast amounts of scarce factor inputs especially land and energy. While, itself creating infrastructure stress through the need to host nearly a million low skilled and lowly paid foreign workers.

And hiding in plain sight is the exposure - nudging the 33 percent limit permitted by the Banking Act (a number conveniently revised upwards when the previously limit was in danger of being busted) of the loan exposures of the 3 domestic banks.

Although real wages have lifted over time, the share committed to real estate - both for a home but also for invesetment (when actually much of this is nakedly speculative as evident by the rapid supply to the resale market of newly launched units. The sucking sound of cashflow hoovered up by property vacuum cleaner has knock on impacts on levels of consumption and retirement adequacy.

Is this pattern desirable? Is it even sustainable? What are the long run consequences? How will it all end?

These are important policy and political questions that should receive more attention before Singapore has its own “China moment”.